Property taxes are not uniform and equal in Nevada

Lost in the shuffle in the last special session was the fact that the state government isn't the only government in Nevada that pays for education. There's a reason the state directly chips in as much as it does, however — and the reason is us and our thoroughly, ruinously California-inspired property tax system.

On the one hand, property taxes don't directly contribute much to the state budget. Of the $7.3 billion collected in taxes by the state in Fiscal Year 2019 (July 1, 2018 - June 30, 2019), the Local Government Finance Redbook for that time period indicated only $203 million — less than 3 percent — would be contributed by property taxes. However, according to the most recent Local Government Finance Redbook, property taxes contribute roughly $1.7 billion to the state's school districts (more than the $1.5 billion allocated to the Department of Education in the state budget this fiscal year), nearly $1.2 billion to county budgets, and over $500 million to city budgets.

Outside of Carson City, in your schools and your cities, property taxes are a big deal. They're what pays the bills when the state can't.

Given how big of a deal property taxes are to local and educational budgets, and given that Article 10, Section 1 of the Nevada Constitution requires the Legislature to provide a uniform and equal rate of assessment and taxation, you might expect property tax rates between neighbors to be… well… uniform and equal.

You might.

In 1978, California passed Proposition 13, a voter initiative that amended the California Constitution, which limited all property taxes statewide to 1 percent of full cash value (how much it might sell for, in other words) and limited annual increases of assessed value on individual parcels to 2 percent per year. The goals were to keep California's taxes low and keep fluctuations in property values from raising property taxes high enough to displace retirees from their homes. Not to be outdone, Nevada's voters also passed a similar measure — Question 6 — in 1978, which contained similar language, as well as an additional requirement that all future tax increases must pass with at least a two-thirds majority.

One difference among several between California and Nevada, however, is that, in Nevada, when voters want to change the Constitution, we have to pass our referenda twice.

There's wisdom in that approach since it gives the Legislature a chance to meet the will of the voters via statute where mistakes are comparatively easy to correct in forthcoming sessions — which, incidentally, is exactly what the Legislature did in 1979 and again in 1981. In 1979, the Legislature passed SB204, which statutorily capped property taxes at $3.64 on each $100 of assessed valuation (Article 10, Section 2 of the Nevada Constitution limits property taxes to five cents per assessed dollar; I suppose the idea of anyone having $100 to tax in 1936 when that article was added may have seemed fanciful at the time). Satisfied with the Legislature's actions, the voters left good enough alone and decided against ratifying Question 6 in 1980.

Why would Nevada's voters be satisfied with a 3.64 percent tax cap when California passed a 1 percent tax cap? The answer is AB168, which passed in 1963 and set assessed value to 35 percent of full cash value. Apply the 1979 cap to the 1963 cap and you have an effective property tax cap of 3.64 percent of 35 percent (1.274 percent) of the market price. It's not 1 percent, but it's still noticeably less than the constitutional maximum of 5 percent of 35 percent (1.75 percent).

Then came the Tax Shift of 1981, which started Nevada's journey towards a much less uniform and much less equal property tax system.

Emboldened by the vote of confidence received in 1980, the Legislature decided to reward voters for their loyalty by cutting property taxes by half (and raising sales taxes to make up for the lost revenue). 1981's SB69 changed the basis for assessing property values from full cash value (again, an estimation of market price for a property, including whatever happens to be built upon it) to taxable value.

Taxable value, according to the Department of Taxation's 2020 Property Tax Elements and Applications, is the market value of the land based on what it's actually used for (instead of what it's legally usable for — an important distinction when you're talking about empty lots in urban areas), plus replacement costs for any improvements upon the land, minus 1.5 percent depreciation for up to 50 years for each improvement. What this meant, and still means today, is that property is taxed based on how much the land underneath it is worth, plus the cost to build a new house on that land, minus however many years of depreciation are applied to the improvement.

One consequence of the switch from full cash value to taxable value is that, since the homes in the Newlands Addition (a relatively upscale and previously segregated neighborhood in old southwest Reno) were all built before World War 2, they are fully depreciated to the tune of just under 47 percent of their replacement value (depreciation, like interest, compounds, but in the opposite direction — each bite of depreciation becomes steadily smaller with time). Because of that, all else being equal, the property tax owed on a $500,000-$600,000 Newlands Addition home will be substantially lower than the property tax owed on a similarly priced home built after the Great Recession.

The final piece of Nevada's property tax puzzle — or the final nail in the coffin, depending on your point of view — came in 2005 with AB439, which finally added the spirit of the second half of California's Proposition 13 to Nevada's statutes. Unlike California's 2 percent annual cap, however, Nevada's was set to 3 percent for owner-occupied single-family homes and low-income housing, and up to 8 percent annually for other properties.

***

Put the pieces together and you have Nevada's current property tax valuation system:

Start with the market value of the land under your home if all of your neighbors did the exact same thing with their land that you're doing with your land. Next, add the replacement value (not the market value) of your home. Then, subtract annual depreciation from the home's value. That's your taxable value.

Now, calculate 35 percent of your taxable value. That's your assessed value.

Then, multiply your assessed value by your property tax rate, which will be no more than 3.66 percent (the Legislature passed a couple of tax increases since 1979 to repay some bonds, which pushed the effective limit above the 1979 statutory limit even though the Legislature hasn't changed or increased the limit).

Finally, if you owned the property you're being taxed on last year, compare that number against last year's property tax bill. If you live there, it's a house, and the number is bigger than 3 percent more than last year's property tax bill, you will only pay 3 percent more than last year's property tax bill. If you don't live there, or it's not a house, and the number is bigger than 8 percent more than last year's property tax bill, you will only pay 8 percent more than last year's property tax bill.

Simple, right?

***

One of the core tenets of Libertarianism is that good intentions aren't enough when discussing public policy.

For example, yes, some drugs are frequently bad for the health and sanity of those taking them and anyone that has to clean up after them. That, however, doesn't justify treating drug users like criminals — as bad as some drugs might be, being labeled a criminal by our government with all that entails (prison time, disenfranchisement, severely reduced access to decent work and housing after serving time, and so on) is demonstrably worse for everyone.

Another core tenet of Libertarianism, of course, is that taxation is bad and should be minimized (if not outright eliminated) as much as possible.

But what happens if we put the two tenets together? Does Nevada's current property tax system reliably produce lower property taxes for all property owners in Nevada?

If the answer is yes, the benefits are neither uniform nor equal.

To understand why, we need to take another look at the state that inspired Nevada's current system. Since Proposition 13's passage in 1978, property values throughout California have skyrocketed due to chronic underbuilding of new housing throughout the state. As a result, new homebuyers in California are assessed and pay 1 percent of the inflated market price. For example, 1 percent of $626,170, the median selling price for single-family homes in California, is $6,261.70, or nearly $522 per month. To put that into perspective, according to the US Census 2018 American Community Survey, the national median rent for a two bedroom residence was $1,044. That means new home buyers in California are, on average, paying the government for half of a two bedroom apartment each month, in addition to whatever mortgage they took out to buy their home.

Those don't sound like low property taxes to me.

Long-time property owners in California, on the other hand, are only assessed for the sale price of their properties when they purchased them plus annual increases of no more than 2 percent each year. Additionally, the capped assessments can be inherited — if a property owner gives their home to a child, for example, the child can inherit the original, lower assessment. Consequently, longtime property owners in some California neighborhoods pay less in property taxes than their newer neighbors — much less, in fact. In some neighborhoods, longtime property owners pay less than 20 percent of what their neighbors pay each year.

Nevada's cap, of course, wasn't put into place until 2005, and the scheduled rate of increase is significantly more than California's 2 percent cap, so we'd expect any distortions created by the cap to be relatively modest. However, per NRS 361.227, taxable value must not exceed market value; after the Great Recession, market values throughout Nevada plummeted. Consequently, many property owners saw their property tax bills drop significantly after 2009, with future property tax increases capped to 3-8 percent increases of significantly lower Great Recession valuations.

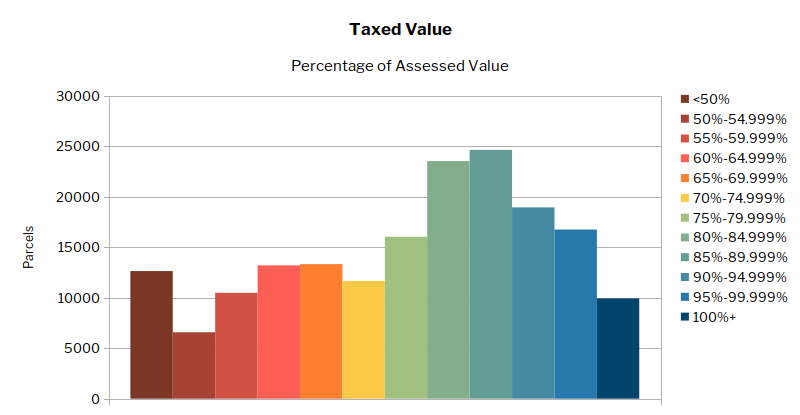

Once the cap and the Great Recession were combined, according to parcel data from Washoe Open Data along with a table of assessed property taxes provided through a public records search to the Washoe County Assessor's Office, Nevada immediately began to experience the same divergence in property taxes between similar properties that California has experienced for decades.

Of the 177,631 parcels listed from the Assessor's Office, 12,632 of those parcels — over 7 percent — are taxed at less than half of their currently assessed value. 47.22 percent of the parcels are taxed at less than 85 percent of their assessed value.

Interestingly, 176 of the parcels with the lowest capped valuations are condominiums in Belvedere Tower, a casino-to-condo conversion that briefly turned into a fiery metaphor of Reno's downtown condominium market in 2008. Before the fire and the Great Recession, Belvedere Tower condos sold for over $200,000. After the Great Recession, however, several condo owners foreclosed, dropping the market price to a small fraction of their original value. Though the market price for condos largely returned before the pandemic, they are still taxed on their post-recession valuations, which are less than 25 percent of their market valuations:

Source: Washoe County Assessor's Office public records search

Another pattern revealed by combining the Washoe County Assessor's Office's billing data with Washoe Open Data's parcel data, meanwhile, is that newer developments are paying much, much closer to their assessed values in property taxes than older developments. This is even true between developments that were built decades ago.

Take, for example, the area surrounding the northeast portion of McCarran Boulevard, a ring road that circumnavigates parts of Reno and Sparks:

The red and orange parcels pay less than 70 percent of their assessed value in property taxes, while the green and blue parcels pay closer to their full assessed valuation. What is the difference between the red and orange block surrounding Probasco Way and the green and blue blocks sandwiching the red and orange block? The red and orange-colored houses were built in the 1960s, while the green and blue-colored homes were built in the 1970s. Consequently, the red and orange homes, which are older, lost more of their value after the Great Recession.

Comparing the property tax valuations for two homes, one from the red and orange block (028-181-21) and one from the green and blue block (028-162-25) demonstrates what happened:

Source: Washoe County Assessor's Office Real Property Assessment Data

Both homes lost value until 2012, where they reached their lowest value. The newer home declined in value from a peak of $128,451 in 2008 to $74,612 — a 42 percent decline. The older home, on the other hand, declined in value from a peak of $100,438 in 2008 to $41,458 — a 59 percent decline. Since then, even though the taxable value of both homes restored most of their pre-2008 value, the tax cap value — the value each property is taxed against — has increased slowly. For tax purposes, the older home is still valued less than it was in 1997; the newer home, meanwhile, is only now getting taxed at its turn-of-the-century valuation.

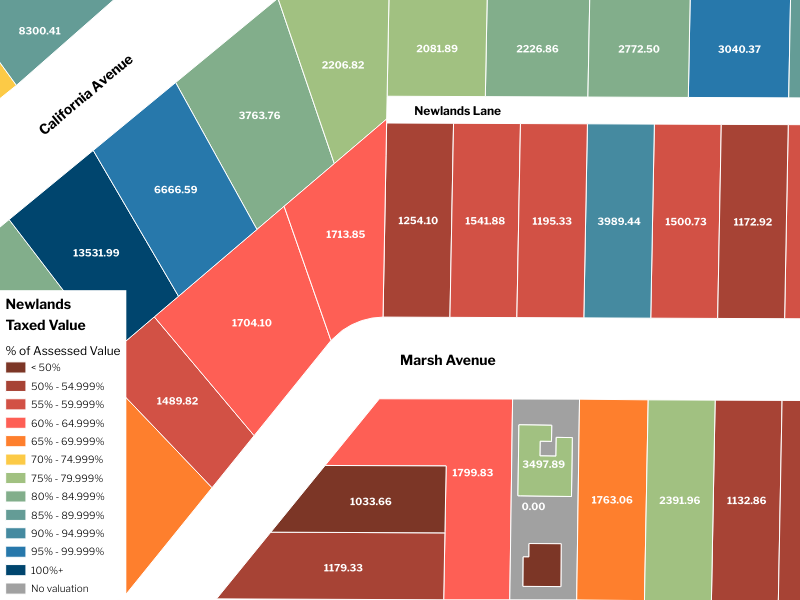

Zooming in on the Newlands Addition, the neighborhood the Reno-Gazette Journal's Anjeannete Damon highlighted on July 20th, we can also see the difference in property taxes paid between older residents and newer residents (numbers on the parcels are their 2020 property tax bill):

The parcel in blue on Marsh Avenue paid nearly $4,000 in property taxes this year. Each of their neighbors, on the other hand, paid less than half of that. There are two reasons for the difference. First, the house on the blue lot was built in 1986, while the house west of it was built in 1941 and the house immediately east of it was built in 1923. Consequently, the houses surrounding the blue parcel are fully depreciated, while the newer house (which is still 34 years old) still has 16 years of depreciation. Second, the newer house was sold to a new owner in 2017, which reset the cap on the property to 2017's valuation; the surrounding houses, on the other hand, were last sold decades ago.

Also note that all the houses on Marsh Avenue are worth over $500,000 each, or at least were before the pandemic hit. At that valuation, the homeowner paying nearly $4,000 in property taxes is effectively paying a 0.8 percent property tax rate. Their neighbors, meanwhile, are paying closer to 0.25 percent.

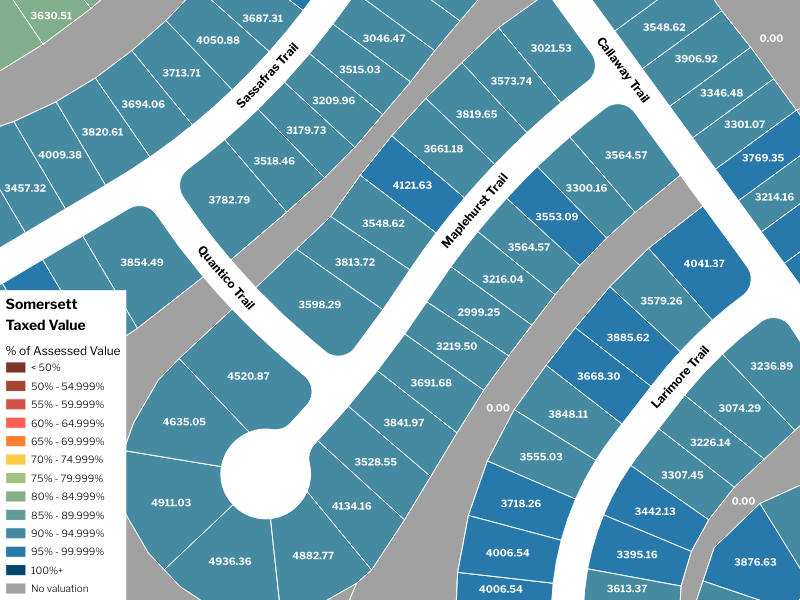

Compare this neighborhood to a neighborhood in Somersett, a new subdivision west of Reno. Home values, as reported by Zillow, are between $400,000-$650,000, roughly similar to the market value of homes in the Newlands Addition. However, because the homes are new, they haven't depreciated much. Also, since they sold after the Great Recession, they're assessed at post-recession tax cap rates. The difference is obvious:

If you ever wondered why Nevada's cities are so desperate to build new subdivisions on the edge of town, that picture is why. Yes, in-fill resets property tax caps, too, but only does so one property at a time and annoys the neighbors. A new industrial-scale subdivision, on the other hand, brings in dozens, hundreds, even thousands of new parcels paying full assessed value on their property tax bill, year after year.

Well, until the next market correction. Then the cycle repeats.

***

The real kicker, though, is that the property tax cap also applies to commercial properties. Take parcel 038-430-02, which paid only 8.08 percent of its assessed valuation in property taxes this year.

Reno residents know it better as Boomtown.

In 2005, it was taxed as a $25 million property. Today, despite having restored most of its pre-recession value, it is currently taxed as a property worth $1.7 million. The result is a nearly $250,000 difference in this year's tax bill.

Though Boomtown might benefit from the greatest difference, percentage-wise, between assessed and taxed value of all commercial properties, it doesn't save the most in pure dollar terms. That distinction goes to the Grand Sierra Resort, which saves over $1.6 million per year on the difference between two of the properties that make up the resort (012-211-28 and 012-211-36). It's not particularly unique in that regard; two properties belonging to the Sparks Nugget (032-172-28 and 032-201-21) saved nearly $500,000 in property taxes this year.

***

I want to be clear about what I'm arguing in favor of here. Do I think Nevadans should pay more in property taxes?

No.

On the other hand, I also believe equality before the law (and before the county assessor) is important as well. Holding property through a recession shouldn't give companies a decade-plus long competitive advantage over companies that buy property after market conditions — and market valuations — improve. Similarly, two neighbors with similar houses should pay similar property tax bills.

To get back to our constitutionally required "uniform and equal" standard of property taxation, we first need to look at California, which has "enjoyed" its cap for over four decades now, and observe that the cap has done nothing to actually keep property tax low. What it's done instead is shifted the burden of property taxation from long-time residents and business owners to new arrivals — or just to long-time residents and business owners with the temerity to move sometime in the past half-century.

Once evictions and foreclosures start in September, Nevada's real estate markets will stop hovering in midair and will crash back to Earth. There's no way they can't — our real estate markets can't continue climbing ever higher when over 15 percent of Nevada's labor force is unemployed. Once that happens, another crop of Nevada's property owners will have their properties reassessed at much lower values, as they should — everyone will be running out of money, taxpayers included, and our tax burden should reflect that.

The problem is what happens after the pandemic and its associated economic dislocations are over.

Now is the time, whenever everyone is going to be paying a little less in property taxes anyway, to decide how things are going to be done when we return to normal and we pave the streets with gold once more. This time, however, I recommend we spend a lot less time copying California's homework and a lot more time reading the Nevada Constitution.

David Colborne has been active in the Libertarian Party for two decades. During that time, he has blogged intermittently on his personal blog, as well as the Libertarian Party of Nevada blog, and ran for office twice as a Libertarian candidate. He serves on the Executive Committee for both his state and county Libertarian Party chapters. He is the father of two sons and an IT professional. You can follow him on Twitter @DavidColborne or email him at [email protected].

Support Independent Elections Coverage and Journalism in Nevada

You’ve enjoyed unlimited access to our reporting because we’re committed to providing independent, accessible journalism for all Nevadans.

But sustaining this work — informing communities, holding leaders accountable, and strengthening civic life — depends on readers like you.

Nevada needs strong, independent journalism. Will you join us?

A gift of any amount helps keep our reporting free and accessible to everyone across our state and funds our elections coverage.

Choose an amount or learn more about membership