A $650 million secret: Why are the Raiders and Bank of America keeping loan details private?

When NFL owners approved the Oakland Raiders' move to the desert in March, a group of laborers celebrated at the famous "Welcome to Fabulous Las Vegas" sign.

They brought silver-and-black posters, banners and flags, giddy with excitement that the casino-speckled city had done what was once unthinkable — secure a professional football team. But in the end, a record $750 million public contribution toward a shiny, new stadium was too good for the league owners to resist.

Members of Laborers Local 872 cheered.

Southern Nevada leaders called it a historic day.

Raiders owner Mark Davis grinned ear to ear.

Meanwhile, the casino magnate who catalyzed relocation discussions by pledging $650 million of his family's wealth toward the project — before backing out two months shy of the NFL vote — was absent the hoopla. Sheldon Adelson's company, the Las Vegas Sands Corp., released only a short statement after the relocation vote:

"As the earliest advocates for the construction of a world-class stadium, which would attract many of the major sporting events and entertainment performances not currently held in Las Vegas, we remain optimistic about the significant economic and tourism benefits the stadium development would provide Southern Nevada."

But it wouldn't be Adelson writing the check. Instead, the billionaire's optimism was resting on Bank of America's willingness to cover the gaping void he created and grant a nine-figure loan to the Raiders.

Several weeks before team owners convened in Phoenix for an annual meeting, the Raiders told the NFL that Bank of America had stepped to the plate as a financing partner, a move that thrust the project, once considered dead in the water, back into the realm of possibility.

The financing arrangement

But both parties have been mum about the details of the arrangement, which includes Davis — widely considered to be one of the least wealthy NFL owners — guaranteeing more than $1 billion in loans without a public understanding or explanation of how they're structured.

Steve Hill, Nevada's top economic development official who chairs the Las Vegas Stadium Authority, said the Raiders' estimated share of the stadium bill would be roughly $1.15 billion. That includes a likely $200 million loan from the NFL, another $200 million expected to be generated by personal seat license sales, $100 million from the team itself and at least a $650 million loan from Bank of America, Hill said.

But NFL team revenue, including the Raiders, can be opaque. While the team's estimated net worth has jumped from near the bottom of teams to 20th according to Forbes, in part because of speculation about a new stadium, credit-rating agencies and public officials generally don't get to peek behind the veil into a team's financial well-being.

Joe Mielenhausen, a spokesman for Moody's Investor Services, said that credit agencies don't typically take a team's revenue into account when rating stadium projects, and that historically most deals that involve fiscally troubled teams don't end with stadiums being repossessed.

"In the case of past team bankruptcies (Dodgers in 2011, Rangers in 2010, Cubs in 2009), the team has typically been sold and the stadium has been fine," he said in an email. "The league can also step in to help the team or may have the right to sell it (depending on the league)."

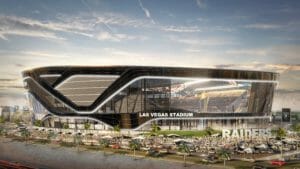

The $750 million public contribution — courtesy of a hotel room tax increase, which went into effect March 1 — brings the financing package up to an estimated $1.9 billion, the number long floated as what's needed to build the planned 65,000 seat stadium.

So what would make a financial institution such as Bank of America eager to step forward and provide the massive loan? After all, Las Vegas may have worldwide brand recognition, but it's the 40th largest media market in the country. The Bay Area, which includes Oakland, ranks No. 6, according to Nielsen data.

Representatives for both Bank of America and the Raiders declined to comment for this story, but a number of factors could be at play. Some have speculated that Bank of America could see it as a way to gain favor with the NFL after Goldman Sachs pulled out of the project along with Adelson. (Goldman Sachs has a long business history with the Las Vegas Sands Corp.) And as ESPN's magazine recently reported, Bank of America has its own history with the Raiders:

"Bank of America was a natural choice: For decades, it has served as the Raiders' bank, and not incidentally, for nearly a quarter century it has also been Jerry Jones' bank and a Cowboys team sponsor," the story states.

Hill, however, characterized it as a straightforward business transaction: "Obviously, Bank of America has spent the time it takes to do the due diligence on this. They feel like it is a solid business opportunity for them and a solid loan to make."

The Raiders bear all responsibility for the loan, Hill said. The county and state would not be held liable if the team defaults on payments, nor would the bank be able to foreclose upon the stadium, he said.

Roger Noll, an economics professor emeritus at Stanford University who has criticized this stadium deal and others, doesn't buy the notion that Bank of America is entering the project as a way to curry favor with the league.

"Bank of America wants to make money," he said. "The NFL wants to make money. The Raiders want to make money."

That's why Noll expects the Stadium Authority, which would own and govern the facility, to come out on the losing end of the deal. The Bank of America loan would need significant collateral behind it, which likely would not include ownership of the stadium or team itself, he said. With the Raiders being the Davis family's main business, Noll said they would be risking everything by agreeing to put team ownership up as collateral for the loan.

What else might give Bank of America enough confidence the team can repay the loan? The promise of revenue streams generated from within the stadium, Noll said.

The Raiders could guarantee the bank money from things such as naming rights, which could yield about $20 million per year, and concession sales, Noll said. Stadium operating companies also enter into agreements with beverage companies for rights to be the only soda or beer provider at the facility — another money-making opportunity that could be directed to help offset the loan.

Those type of terms would be outlined in the lease agreement, which is why Noll suspects the Stadium Authority may wind up receiving zero — or very little — revenue generated from within the facility.

The Raiders submitted a draft lease agreement to the Stadium Authority in January, which drew considerable public criticism because the team suggested it only pay $1 annually in rent and receive revenue from naming rights for the facility and any adjoining plaza. Last month, the Stadium Authority discussed the lease agreement with the Houston-based attorney retained as its counsel.

The Stadium Authority has not approved a lease agreement with the team yet, but the board meets again Thursday and will receive an updated draft. Staff will give the board a progress report on findings and document approvals required for the project.

Per a provision in the legislation that authorized the room tax increase and created the Stadium Authority, the nine-member board must also determine the development partners have the financial wherewithal to take on the project.

The relative silence concerning the lease agreement in recent weeks could be an indication that the Stadium Authority and the Raiders haven't hammered out a solution to their competing interests, said Noll, who co-authored "Sports, Jobs and Taxes," which explores the economic impact of stadiums and sports.

"I think there's an unresolved disagreement that's bubbling below the surface," he said. "The lack of transparency allows it to continue to bubble below the surface."

Silence not unusual

Looking at how other teams financed their portion of stadium costs doesn't necessarily provide much clarity, either. The Minnesota Vikings put $609 million toward U.S. Bank Stadium, which opened last year, through a combination of private financing and equity, a $200 million NFL loan paid back through stadium revenue and $100 million in net proceeds from personal seat licenses. A Vikings spokesman said the team has not disclosed the breakdown of private financing and equity.

Sports economist Tim Kellison, who studies stadium financing, said banks are usually willing to enter into stadium construction financing deals with major sports teams because of their perceived fiscal successes, though the actual books tend to remain private.

"The banks are not just throwing out huge amounts of money without doing a real deep dive into the financial forecasts, and what's already in the books," he said "I still think it's kind of a safe investment, relatively. The NFL has been around for a long time."

Kellison, who grew up a Raiders fan, said policymakers and those involved with the stadium discussions have reason to be optimistic about the team moving to Nevada, but he cautioned that trying to forecast 30 years of economic activity covering the proposed life of the stadium was near impossible.

"I don't think Las Vegas will be immune if another recession hits," he said. "That's something to think about, to worry about. Anytime public money is involved, there's all these contingencies that aren't planned for."

Despite the murkiness surrounding the Bank of America loan, the financial institution's apparent willingness to participate gives Clark County Commission Chairman Steve Sisolak — who helped shepherd the project through a year-long process — a peace of mind about the project's viability.

"If anything, it gives me a greater sense of confidence because I know banks are conservative and would not take a risk on something like this," he said.

Feature photo caption: The Las Vegas Strip is seen Monday, April 10, 2017, while traffic travels near Interstate 15 and Russell Road. Photo by Jeff Scheid.

Support Independent Elections Coverage and Journalism in Nevada

You’ve enjoyed unlimited access to our reporting because we’re committed to providing independent, accessible journalism for all Nevadans.

But sustaining this work — informing communities, holding leaders accountable, and strengthening civic life — depends on readers like you.

Nevada needs strong, independent journalism. Will you join us?

A gift of any amount helps keep our reporting free and accessible to everyone across our state and funds our elections coverage.

Choose an amount or learn more about membership